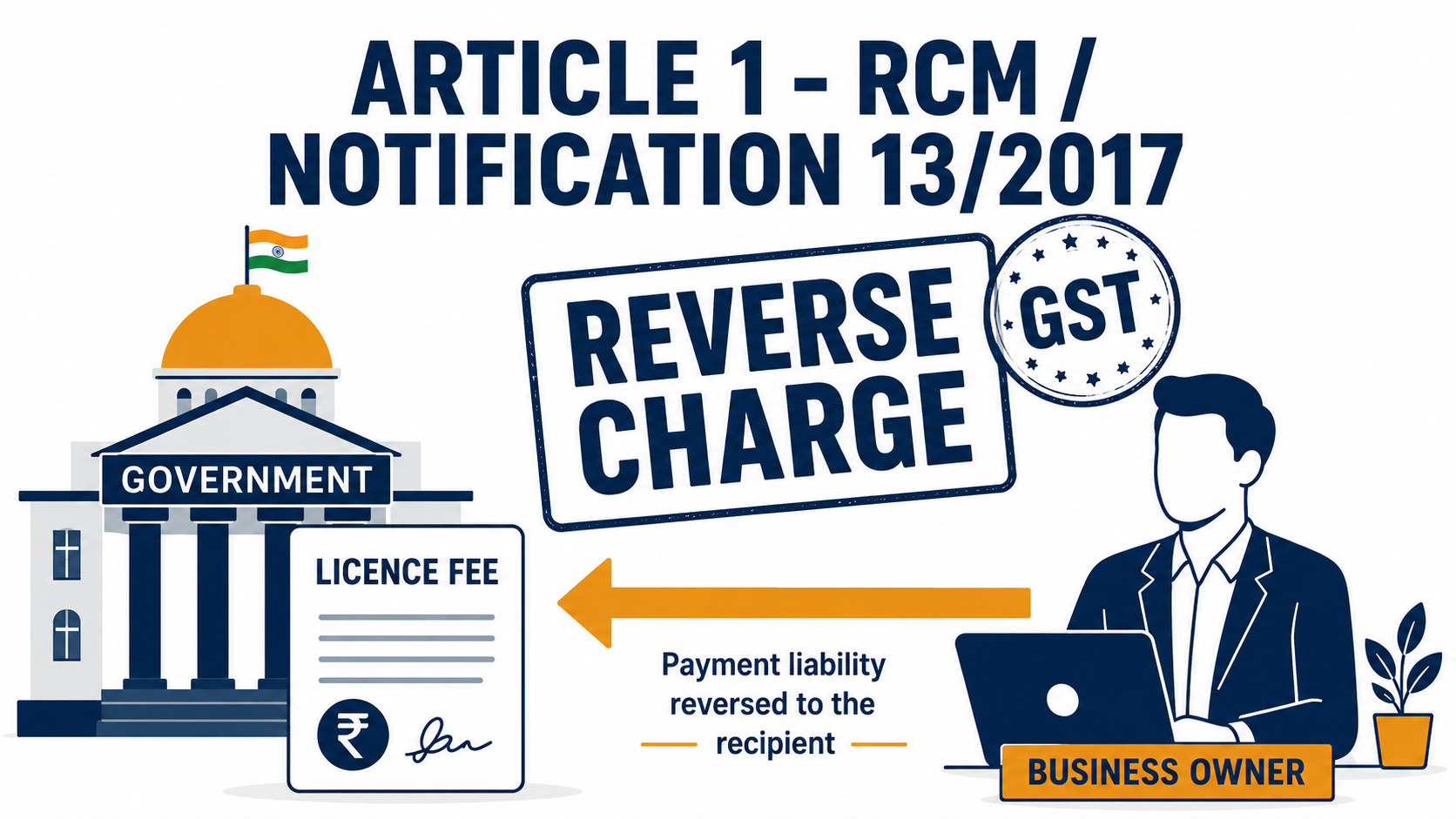

What Is the Reverse Charge Mechanism?

Normally, the supplier of a service collects and pays GST. Under RCM, this responsibility flips — the recipient of the service pays the GST directly to the government, regardless of whether the supplier has charged it. The legal basis is Section 9(3) of the CGST Act, 2017, which empowers the government to specify categories of services where GST must be paid by the recipient.

What Is Notification 13/2017-CT(R)?

This is one of the key GST notifications issued under Section 9(3). It lists specific categories of services on which GST is payable under RCM. The most commonly encountered ones:

| No. | Category of Service | Supplier | Recipient Liable |

|---|---|---|---|

| 1 | Goods Transport (GTA) | Goods Transport Agency | Specified recipients |

| 2 | Legal services | Advocate / Firm of Advocates | Business entity |

| 3 | Arbitral tribunal services | Arbitral Tribunal | Business entity |

| 4 | Sponsorship services | Any person | Body corporate / Partnership firm |

| 5 | Services by Government / Local Authority | Central/State Govt./Local Authority | Business entity |

| 6 | Director services | Director | Company / body corporate |

| 7–9 | Insurance agents, recovery agents, copyright | Respective agents/authors | Insurance companies, banks, publishers |

Entry No. 5 — The Government Services Entry (The One That Trips Most Businesses)

Under Entry No. 5, services supplied by the Central Government, State Government, Union Territory, or Local Authority to a business entity are taxable under RCM. This includes:

- Mining royalties

- Government testing fees

- Licences, permissions, and approvals issued by government departments

So if a government department issues your business a licence or permission in exchange for a fee, you are generally liable to pay 18% GST on that fee under RCM — even though the government is the one receiving the payment.

Does Every Government Payment Attract GST?

No. The key question is: is the government providing a service, permission, or right in exchange for the payment?

| Payment Type | GST Under RCM? |

|---|---|

| Income tax / Customs duty | No GST |

| Penalty / Fine | Usually No |

| Licence fee for a permission or right | Generally Yes |

Taxes, penalties, and statutory levies are not "consideration for a service" — so they fall outside the scope of GST entirely.

When Is RCM Not Applicable?

- Services by Courts / Tribunals — Not taxable

- Functions under Article 243G / 243W (Panchayat / Municipality) — Exempt

- Services to non-business individuals — Usually not under RCM

- Tax, penalty, or statutory levy — Not consideration for a service

- Sovereign functions specifically exempted — No GST

Can You Claim ITC on GST Paid Under RCM?

Yes — if the service is used in the course or furtherance of business, the GST paid under RCM is generally available as Input Tax Credit (ITC), subject to the conditions under Section 16 of the CGST Act.

The Bottom Line: Not every rupee paid to the government attracts GST. But if your business is paying fees for licences, permissions, or rights granted by a government body — there is a strong likelihood that RCM applies and you are required to self-assess and pay GST on that amount.

Unsure whether a specific government payment triggers RCM for your business? Reach out to ASA and Company for a free consultation. A quick review with your CA can save you from notices and penalties later.